Webinar Date: Thursday, February 8, 2024 | 2:00 pm EST

The landscape of Know Your Customer (KYC) protocols has changed drastically over the last decade and a half. It’s fascinating to witness a shift from general reluctance towards KYC implementation to its widespread adoption across various sectors today. During our recent webinar, only 3% of participants had no form of KYC in place – a testament to its growing acceptance.

KYC now serves a variety of critical purposes, including enhancing fraud prevention measures, ensuring regulatory compliance, bolstering customer security and improving customer support. Remarkably, the majority of our webinar attendees reported using KYC for all of the above. Despite these advances, the journey of KYC’s evolution is far from complete, and there still remain several opportunities for further development.

This blog will dive into one of the key challenges faced in KYC: the challenge of adequately serving thin file populations. I will explore the potential hidden within these groups and the untapped opportunities they present. Additionally, I will highlight some of the most effective KYC tools and techniques worth considering. To wrap up, I will provide an overview of upcoming trends within the regulatory landscape, offering insights into the future direction of KYC practices.

Challenges in thin file and no hit populations

Navigating the verification process for new customers presents its own set of challenges, especially when it comes to individuals from different backgrounds or lifestyles who may want to access financial services. The process of verifying customers isn’t always straightforward, and some demographic groups prove to be more challenging than others.

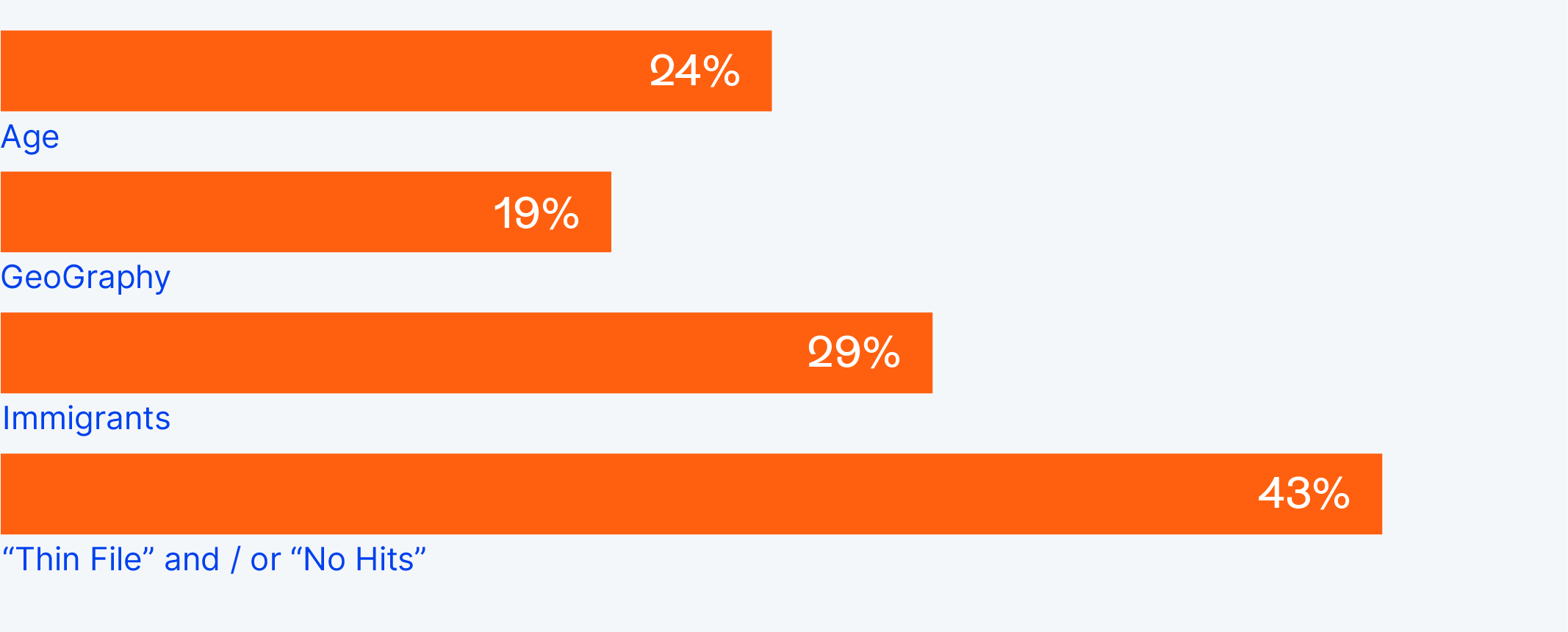

Feedback from our webinar attendees underscores this issue, highlighting that thin file and no hit populations represent some of the greatest challenges in the customer verification process.

What demographic challenges do you face in verifying new customers?

The Consumer Financial Protection Bureau (CFPB) defined thin file populations as people with a limited number of credit relationships, and therefore, an insufficient credit history to create a credit score. Thin file populations make up 8.3% of the entire U.S. adult population, representing 19 million Americans. The number is even greater among the no hit population, which consists of those who do not have a credit history at all. This population makes up 11% or 26 million of the total U.S. adult population.

Combined, 45 million Americans are unscorable or credit invisible, meaning they cannot access quality credit and may struggle to get verified or approved at financial institutions.

Thin file and no hit populations present complex risk management dilemmas for fraud prevention teams, often leading to a heightened scrutiny that may unjustly penalize legitimate individuals. The friction and frustration might drive these potential customers away, either abandoning the process or turning to competitors.

This poses a significant customer experience and revenue issue that is tied to nearly 20% of the U.S. adult population. Due to the sheer volume of this group, many of its users will inevitably end up in your customer funnel. Therefore, it is critical that when legitimate customers from this group do decide to build a credit relationship, the proper risk management tools are in place to enable them, rather than push them away. Many members of these underserved and protected populations already face enough biases as it is, so it is especially important to double down on creating a positive user experience.

Tools and techniques to explore

The more data points you have available, the easier it becomes to distinguish between legitimate and fraudulent users – even those in thin file or no hit populations. Relying on traditional information sources, such as credit bureaus, is insufficient, but many more alternative sources of information can be aggregated to obtain a high-enough level of confidence that we’re dealing with a real person (and not a synthetic identity). The only thing left is making sure that the information is presented by its legitimate owner.

This is where using strong geolocation data and device fingerprinting can help you stop fraudsters, and lower the risk for legitimate customers.. If you are able to tie someone’s address to where they are actually located, you can significantly reduce risk without the need to outright decline potential customers. This approach also provides additional proof points for underserved or protected users who may not have as much information on file. On the other hand, if many requests are made from the same devices or the same location, you know where to focus your investigation efforts.

Geolocation is especially crucial, as IP alone is not sufficient to make an informed decision. In addition to being spoofed easily, IP addresses can be inaccurate by thousands of kilometers, making them easy to manipulate. In highly regulated markets such as the US iGaming industry, relying solely on IP addresses for location verification isn’t even considered an acceptable method. This trend is likely to extend to other industries, such as the cryptocurrency sector. The Binance controversy highlighted that IP addresses alone were inadequate in blocking bad actors.

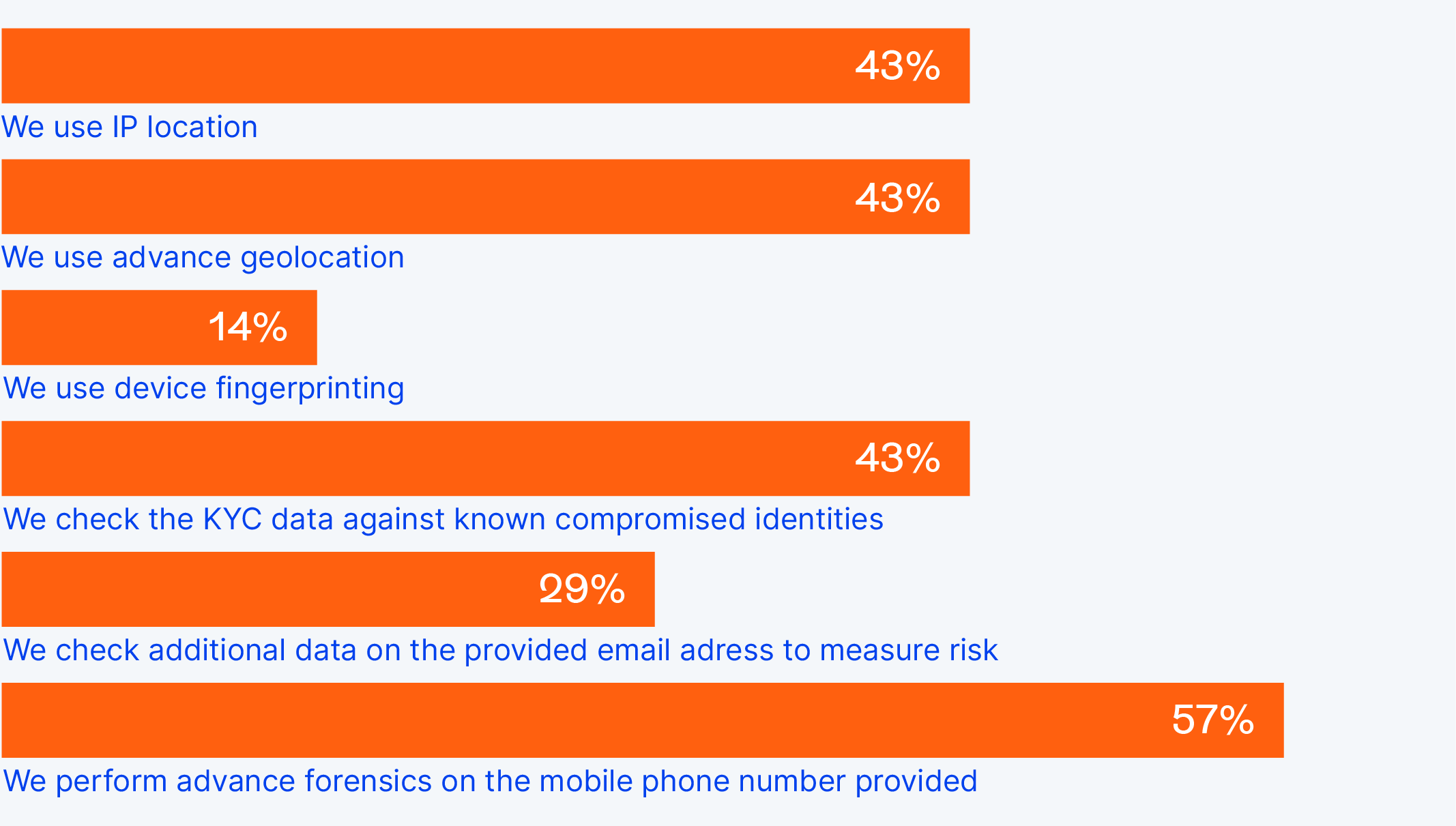

The important role of geolocation in fraud prevention was evident in our poll on KYC tools, where it revealed that 43% of our audience uses advanced geolocation to perform anti-fraud checks.

Are you using KYC tools to also perform anti-fraud checks?

In addition to advanced geolocation, other data points, including emails, phone numbers, SIM information, device data, criminal records and user patterns, are crucial in removing fraudsters from your platform and onboarding more legitimate thin file or no hit users. Checking compromised identities, incorporating device fingerprinting and working with reliable tools and partners will also contribute to the success of your risk management flow.

The 2024 regulatory landscape

Age verification requirements

Quite a lot has already happened last year in the regulatory landscape, and this year is no exception. This is particularly true at the US state level. 2023 saw plenty of action surrounding age verification in multiple states including Arkansas, Louisiana, Mississippi, Montana, Texas, Utah, and Virginia. Discussions around this topic are expected to continue in 2024, especially for adult content platforms. Age verification requirements will push for stronger identity verification measures, which will require geolocation and other ID verification systems.

This is especially true as the use of VPNs has skyrocketed following the introduction of age requirements by various states. Having IP detection alone will no longer be sufficient for accurately verifying a user’s true age or identity.

With that being said, we are also seeing some pushback on age requirement laws due to concerns surrounding the First Amendment. As states continue to enact age requirements for certain platforms, age verification concerns may continue to be challenged.

Anti-money laundering (AML) requirements

Anti-money laundering is a hot topic across multiple countries. Particularly in the U.S. and the UK. As of 2024, in the U.S., businesses are now required to report ownership stakes to prevent money laundering. In the UK, the liability for financial fraud has been moved to the financial institutions rather than the victims. Both of these measures will incentivize institutions to invest in better AML and fraud prevention measures to prove to regulators that they are doing enough.

These actions in the U.S. and the UK are also likely to impact Canada, which has historically been somewhat slower to advance in the AML space. However, 2024 is anticipated to mark the beginning of an enhancement in AML rules and regulations within Canada, aiming to align with international standards and offer greater protection to its consumers. While these regulations might not be fully implemented in 2024, discussions on fraud prevention are already underway, with expectations for more comprehensive regulations to emerge in 2025. Notably, Canada is poised to adopt a unique approach to technological requirements, given that its banking sector falls under federal jurisdictions.

2024 is set to be a significant year on both regulatory and technological fronts. Given the complexities associated with thin file populations and evolving regulatory and technological advancements, it will be crucial to understand the questions you need to answer in order to build your KYC strategy and onboarding process. This includes considering regulatory requirements, (ex. Do you need to verify someone’s age or location?) as well as fraud detection aspects (ex. What fraud signals do you need to take into account and what is your threshold?).

Most importantly, the early collection of diverse data points during the KYC process is vital. It equips you with the necessary insights to make well-informed decisions, enhancing the effectiveness of your fraud prevention measures and regulatory compliance efforts. This proactive approach to gathering comprehensive data from the outset will be instrumental in navigating the evolving landscape of 2024 successfully.

Elevate your digital KYC strategy

Want to discover how our multi-award-winning KYC solution can enhance your compliance and fraud prevention strategy?

About GeoComply

GeoComply provides anti-fraud and cybersecurity solutions that prevent and detect fraud and help verify a user’s true digital identity. Trusted by leading brands and regulators for over 10 years, the company’s geolocation solutions are installed on over 400 million devices and analyze over 12 billion transactions every year. Specializing in compliance-grade geolocation technology, GeoComply offers AML, compliance and fraud solutions for the banking, cryptocurrency, payments, iGaming and media and entertainment industries, building an impressive list of customers, including Akamai, Amazon Prime Video, BBC, DraftKings, FanDuel, BetMGM, Sightline Payments and over a hundred more companies globally.